Intelligent Monitoring Group Limited ($IMB.AX) - Inconsistent behavior

After some significant changes, it’s time for an update.

First of all, the disclaimer: I am invested in Intelligent Monitoring Group ($IMB.AX). Nothing I write should be considered investment advice.

Some of you might be surprised that I waited this long to provide an update on this investment thesis. However, given the significant volume of news, I wanted to ensure that we had a comprehensive view of what did and didn't happen.

Currently, there are three issues I see with the stock, and I want to be as transparent as possible about my thoughts. Be sure to read until the end to get the full picture.

1. Inconsistency regarding guidance

In my previous update, I mentioned two potential catalysts for the stock price: the refinancing and the FY25 guidance at the AGM. To the surprise of all shareholders, they didn't even mention the guidance at the AGM. What followed was a falling stock price, a trading halt, and an equity raise. All of this happened while the majority of shareholders still had no idea what the guidance might look like.

On November 7th, they finally released the guidance, which came in below the previous pro forma EBITDA level of $40.2 million, at just over $38 million. In the equity raise presentation, they explained that FY24 benefited from a one-off impact due to 3G conversions. But what does that actually mean?

When IMB acquired ADT, the previous owner had already committed to upgrading alarm systems from 3G to 4G at price points IMB typically wouldn’t have agreed to. When IMB took over, they priced the new systems to be cash-neutral but were still obligated to deliver the pre-committed upgrades. This resulted in $16.3M in CapEx and a $3M cash loss.

ADT had previously capitalized such costs and amortized them over five years, and IMB initially applied the same approach for the pre-committed systems. However, IMB no longer uses this method for new systems and has transitioned to handing over the pre-committed systems to customers, thereby ending this practice. Spreading costs over five years while recognizing revenue immediately boosts EBITDA, even though it has a negative cash impact in this case. Last year, the positive impact on the P&L was $7.9M.

The transition is now mostly complete, with only 3,000 out of 50,000 customers still on 3G. These customers either didn’t respond to outreach or don’t mind, as 3G is still operational. Essentially, their entire staff was focused on the transition during the last fiscal year. According to the company, they are now fully committed to lead conversion, aiming to generate actual cash flow and profit. So now, without the one-off effect from the transition, they are starting from a lower EBITDA base but anticipate growth from this point forward.

So, that’s the company’s explanation, and I have to admit it makes sense from an accounting perspective. But that’s not the issue here—at least from my point of view. The real problem was their communication. If you look at their results release from August 30th, there was one specific bullet point that made me very bullish about FY2025 and the guidance at the AGM.

I don’t know if it’s just me, but would you have expected lower guidance after such optimistic-sounding comments? They literally mentioned that they’re trading above the upgraded pro forma level of $40.2M.

I don’t want to make unfounded allegations, but one might assume they realized late that the method of expensing costs would have a negative optical impact on their EBITDA. Some believe they withheld guidance as long as possible to keep the stock price stable enough to complete the raise.

This is precisely the kind of behavior I aim to avoid when investing in a stock controlled by a larger investor. It seems as though they deliberately withheld information from us while discussing the raise with larger institutional investors and disclosing the guidance in the term sheet.

They could have easily explained the EBITDA issue beforehand. Yes, it’s possible the stock price might have dropped as a result, but the current price reflects their inconsistent behavior and a loss of trust, which, in my opinion, carries far greater weight.

2. Apparent change in strategy

When I first invested in IMB, it was because management stated they wouldn’t become a ‘typical’ roll-up (Although I initially referred to it as a roll-up in my write-up). Initially, the plan was to grow organically, take an opportunistic approach to acquisitions, reduce debt, and eventually return capital through dividends or buybacks. However, with the equity raise, another acquisition, and a pipeline of five more, the strategy now seems to have shifted toward empire building.

Sure, they never ruled out further acquisitions, but it was never clear to me that they would pursue them at this scale. I recently asked Dennison Hambling a question about the apparent strategy shift during a Q&A, and his response sounded different from before. Technically, he didn’t push back on the claim but instead emphasized that they wouldn’t fail like ‘other’ roll-ups. To me, that wasn’t particularly convincing.

Of course, I understand the rationale behind the acquisitions. Australia is vast, and if you want national coverage to attract enterprise customers, acquisitions act like a fast-forward button.

However, when they talked about bringing this segment back to $130+ million in revenue, I expected most of that growth to come organically. That’s not to say they aren’t growing organically—recently, they mentioned a new contract with a major customer and others in the pipeline.

Roll-ups are always risky. Too often, companies struggle with integration, and it can take years before failures become evident, even as issues grow silently in the background. Dennison might argue that they were indeed successful in achieving this integration. Merging systems and control rooms is a complex task, as it involves integrating technological infrastructure and workflows. For example, they apparently successfully integrated the ADT residential customer base into Signature Security. However, merging people and contracts tends to be comparatively easier to manage. This approach aligns well with their most recent acquisitions and the current pipeline, which seem to reflect this strategy effectively.

From a shareholder perspective, roll-ups come with another risk: the perpetual promise of a bigger company with synergies on the horizon, while management keeps presenting one one-off expense after another. Whether these companies will ultimately achieve profitability remains uncertain.

3 Market dynamics matter

I don’t usually stay invested in a stock for long. I look for stocks that are on the verge of an inflection point and poised for multiple expansion. IMB was in a positive loop, but that’s clearly been broken now.

If you read the comments in various forums, Twitter etc. it’s evident that investors no longer trust the management, and that’s a significant issue for a stock. Without trust, it’s unlikely we’ll see a similar multiple expansion anytime soon.

So why do I stay invested?

To put it simply, because I believe in the company’s assets. This is the first time since they acquired ADT that they have the staff available to actually do lead conversion and show real growth and cash flow, as the transition to 4G is essentially completed.

I could show you again how undervalued this company appears based on adjusted EV/EBITDA, EV/FCF, or P/E multiples, but that only holds if they actually meet their guidance—a reliability I wouldn’t count on anymore. From now on, I’ll would focus less on what management says or how reasonable their adjustments seem, and more on what the financials actually show. You can decide for yourself whether to take their words at face value. It all sounds appealing (growth in Residential, growth in Commercial), but I believe the market now wants to see tangible results in their books.

This means delivering real EBITDA, cash flow, and organic growth.

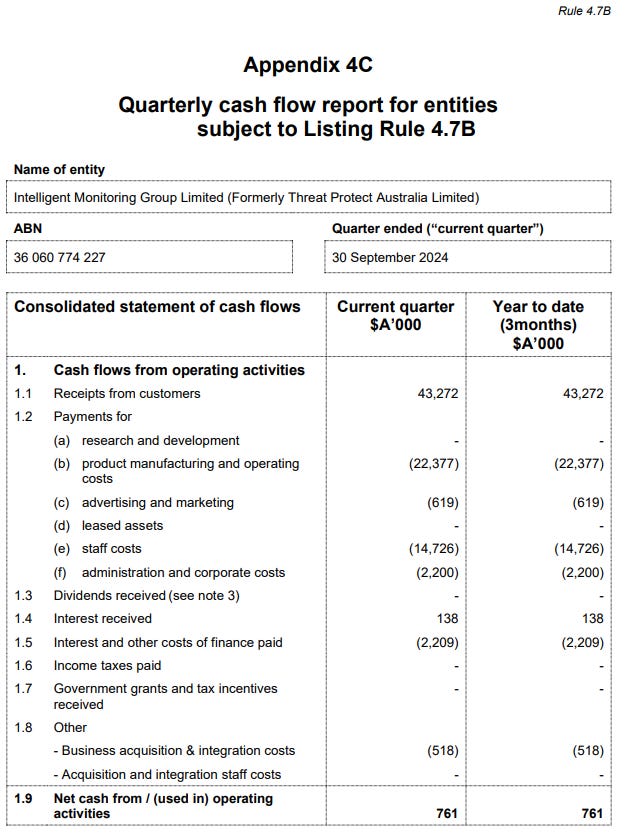

Aside from the acquisition costs for DVL, there shouldn’t be any significant additional one-offs, so this time, they should at least present a larger operating cash flow compared to the previous quarter.

They’ve already communicated the need to allocate $5M in CapEx for the 3G transition in New Zealand, which was outlined from the beginning, so it would be surprising to see real FCF this time. Management has also indicated that profitability and cash flow will be weighted towards the second half of the fiscal year, which might come across as moving the goalposts.

Another point to note is that Q2 will likely show lower revenue, as Q1 still benefited from transition-related one-off effects. This doesn’t necessarily have to be a significant blow to the investment case because it aligns with what they’ve stated. They mentioned that one-off revenues were tied to the transition, which is now largely complete, making it reasonable to anticipate lower revenue in Q2. I just want to clarify what to expect in the next quarter, leaving it up to you to assess how the market might interpret those results.

Does Black Crane no longer have confidence in the stock?

Obviously, we can't say for sure, but based on comments I read after the equity raise, many people were concerned about BC losing confidence, selling more stock, and thus putting pressure on the stock price. Let's evaluate how strong this argument is using the current public information.

BC sold 11% of its position, equivalent to 15 million shares. They still own 37% of IMB and have committed not to sell any additional stock in the next six months.

It’s fairly obvious they intended to sell at the higher prices seen before the AGM. So, I wouldn’t argue that selling at 48 cents signals a lack of confidence. They likely ‘had’ to sell at these levels because they were trapped as the market drove the stock price lower, and their brokers pressured them to complete the raise. I want to emphasize that this is purely my perspective. Since we don’t have any official statements from BC, it’s reasonable to fill the gaps with plausible assumptions.

So, why did they likely sell? It’s important to remember that BC is a fund, not a family office. Funds sometimes need to demonstrate liquidity to their clients. Additionally, the investment in IMB has already exceeded BC's typical timeframe and represents an unusually large position for them.

Again, this is purely my perspective, but given that they still own 37% of the company, I don’t think it would be wise to signal a lack of confidence while selling only 11% of their position without a clear plan. BC can’t easily exit this stock—that much is certain. I’m not entirely convinced by the ‘We want to get into the ASX 300’ narrative, but if that’s accurate, BC would need to sell more shares. However, it seems unlikely they would sell on the open market, as any change in control exceeding one percentage point would require disclosure and could take considerable time, likely exerting negative pressure on the stock price. Perhaps we should instead consider how they sold the 15 million shares this time.

If they truly intend to reduce their position after the six-month period—which seems likely given their stated goal of entering the ASX 300—they would likely follow the same approach as they did this time.

They sold their shares to new and existing institutional investors, which at least demonstrates confidence from the other large existing shareholders. We can’t be certain if MAF and AG purchased shares directly from BC or simply participated in the raise, but MAF increased their position from 5.11% to 7.54%, and AG from 9.58% to 13.22%. Clearly, IMB has the support of its other large shareholders. Those who assume BC lost confidence based on selling stock would need to reach the opposite conclusion regarding MAF and AG.

One factor that could have an impact—at least in the short term—is the share purchase plan, which allows AZ and AU residents to buy stock at a discount to the current market price until November 29. As a result, I assume smaller shareholders participating in the plan are unlikely to purchase shares on the open market before this date.

Conclusion

I believe I’ve been very open about the issues here, and while I want to emphasize that I can’t offer advice, I want to stress again that it’s now about what they can actually demonstrate in their books. That’s why I didn’t include a calculation based on adjustments this time, as they’ve shown themselves to be a company that needs to prove they can deliver.

I asked myself if I made any mistakes at the beginning, and yes, I did. I made this a 9% position from the start, which I usually avoid because I prefer to see a company deliver first to build confidence. I saw some significant catalysts ahead, and the management’s bullish communication fooled me.

That said, I’d still buy into this kind of setup again at any time. Given that the stock is still up 57% since my initial buy at the end of May, one can’t say I was completely wrong with my assumptions regarding the setup—although we don’t know what surprises lie ahead, in one way or another.

I’ll ignore both extremes—the ones calling me naive for buying a company that doesn’t show a profit according to accounting standards, and those putting me in the 'weak hands' basket for selling what they perceive as a temporary blip.

It’s also wrong to say 'everything is as before,' because it isn’t. I based my calculation on EBITDA guidance that no longer applies, and my calculation of maintenance capex seemed—and still seems—to be correct. From my perspective, the stock is more expensive than it was before, at least based on the stock price at the time of my last update. The other key factor here is trust in management. I’ll repeat myself: They have to show they can actually deliver

Agree. Some strange events and for mine a huge withdrawal from the bank of goodwill. Dennison no longer appears so confident. Yes, they now need to prove they can do as they say they can. I was going to seek max retail participation in two of my portfolios, but won’t. I’m sitting back waiting to see how they integrate and put the new debt arrangements in place. This should have been handled more cleanly. Right now it looks like a pea and thimble trick.